Source of data in the image: World Bank, stocks traded, turnover ratio of traded shares.

When asked about who should govern companies, the most obvious answer seems to be: the shareholders. And the reason: because they are the owners. Period. Debate closed. Recent discussions about the increased role of other stakeholders, be they the workers, representatives of external interests such as those of the environment or of suppliers, are seen like nice add-ons, little more than an inflexion to a generally valid rule.

I disagree, and believe that the role of the shareholders in the governance of companies should be radically reconsidered.

What is indeed the reason why the owner of an asset, whatever that asset is, is considered as the best placed to decide about its future? In my views, essentially because that owner traditionally was the steward of the long-term interests of that asset. S/he guarded the asset’s long-term interests, because the asset was very illiquid (i.e. could not be sold easily), and because the person owned that asset for his/her whole life – and transmitted it to the next generation. The most obvious and frequent application field of this behaviour was arable land, in a continent like Europe where the world is “closed”, and there is no additional land to colonise or to clear from forests in case the land is exhausted. Ownership was thus associated with careful management, and with the preservation of the (economic, social and environmental) value of the asset.

I argue that preserving the value of assets serves the public good. Indeed, collective welfare stems from the usage of all forms of capital (arable land, infrastructure, institutions, technological knowledge, equipment, machinery…). This is what makes life in a developed country materially more comfortable, compared to a developing country, at equal levels of GDP: the “old” developed country relies of a wealth of accumulated assets which provide amenities and welfare at a fraction of the cost necessary to set them up in the first place, because maintaining an asset costs far less than building it from scratch. The sewer system is a typical example of an infrastructure that lasts for centuries, and provides welcome amenities for all once built.

In this public good perspective, it is thus legitimate that the public authorities protect the rights of those that are the stewards of the long-term interests of assets.

This applies also in the case of a company. Traditionally, the owner was the stable reference with the long-term perspective of transmitting his/her business over generations, whereas the employees came and went, also because of their highly precarious employment relationship (generally as daily labourers). This is why legislation provided the owner with the sole legitimacy to take decisions.

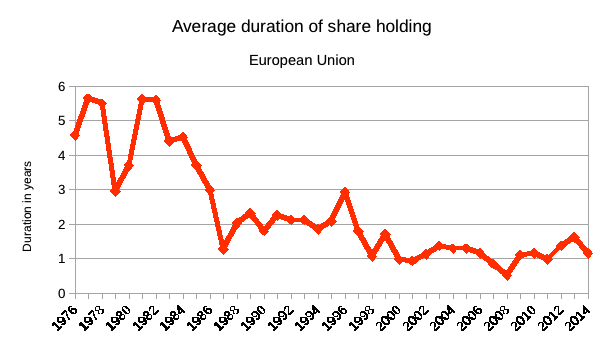

All this justification remained essentially valid until the advent of the limited company with shares tradable on a liquid Stock Exchange market. In such companies, the average duration of share holding has been around one year in the European Union between 1998 and 2014 (last value known) – and decreased from a value superior to 5 years in the 1970s.

Under these circumstances, there can be no claim that the shareholders represent the long-term interests of the company. Their horizon is short, extremely short. If given the choice between (1) a quick run after having stripped the company from part of its assets (or by refusing to maintain them), and (2) the patient build-up of company value, the typical shareholder takes the first option. Forget about “business ethics” here.

As an element of comparison, the average tenure of employees in the EU hovered around 10 years in the years 2004 – 2012 (source EuroFound, 2015).

The traditional situation of the 19th century, where the employee was a daily labourer hardly related to his/her work place, and the (land or company) owner held his position over generations, is completely reverted.

I contend that the public good argument, whereby the stakeholder with the longest interaction with the asset is legitimate to govern it because s/he is the steward of its long-term interests (and thus of a society that collectively relies on the preservation of these assets), remains fully valid. The consequences to be drawn in terms of company governance are rather radical: short-term shareholders should have almost no say, whereas long-term stakeholders, whatever their legal connection to the company, should have a much more determinant role to play.